- US stocks rally to another record high close, dollar quiet

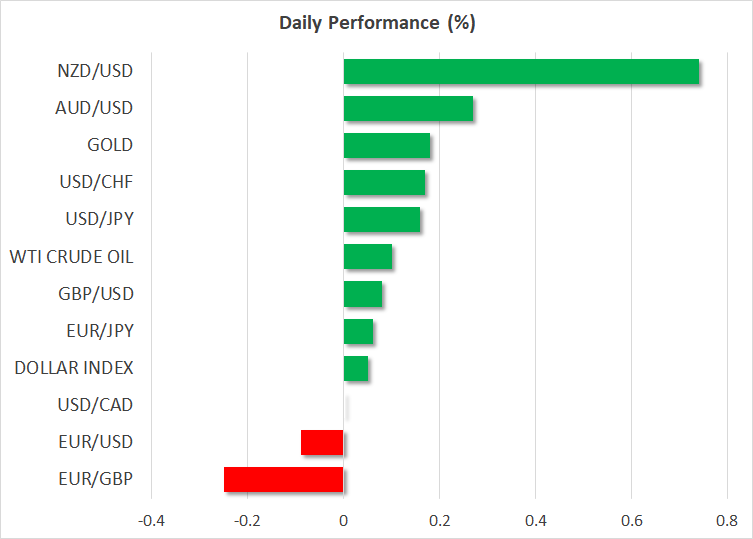

- Kiwi skyrockets after stellar jobs data fuel RBNZ bets

- Gold lifeless, oil takes another hit amid demand worries

Stocks cheer as earnings season delivers

Stocks cheer as earnings season delivers

Wall Street continues to defy gravity. The S&P 500 cruised higher to close at yet another record peak yesterday, telling a much different story than the bond market, which has been feeling the blues lately.

Worries that the Delta outbreak will take the wind out of global growth have been eclipsed by a sensational earnings season and hopes for more federal spending, reigniting the relentless bid in equities. And with global yields sinking – cementing bonds as an asset class with negative real returns – there is simply no alternative to stocks.

Overall, the outlook for equity markets remains promising. Valuations have corrected a touch with earnings going through the roof, the economic recovery is humming along nicely, and a multi-trillion dollar reconciliation package from Congress doesn’t seem to be priced in yet.

The only real risk is the Fed normalizing monetary policy. Markets seem positioned for a tapering announcement around year-end, so if the Fed gets the ball rolling in September already as Waller suggested recently, that could come as a ‘surprise’. Even in this case though, any selloff will likely be short-lived. Stimulus will be dialed back extremely cautiously. The last thing the Fed wants is to shock the market.

Kiwi soars as RBNZ rate bets mount

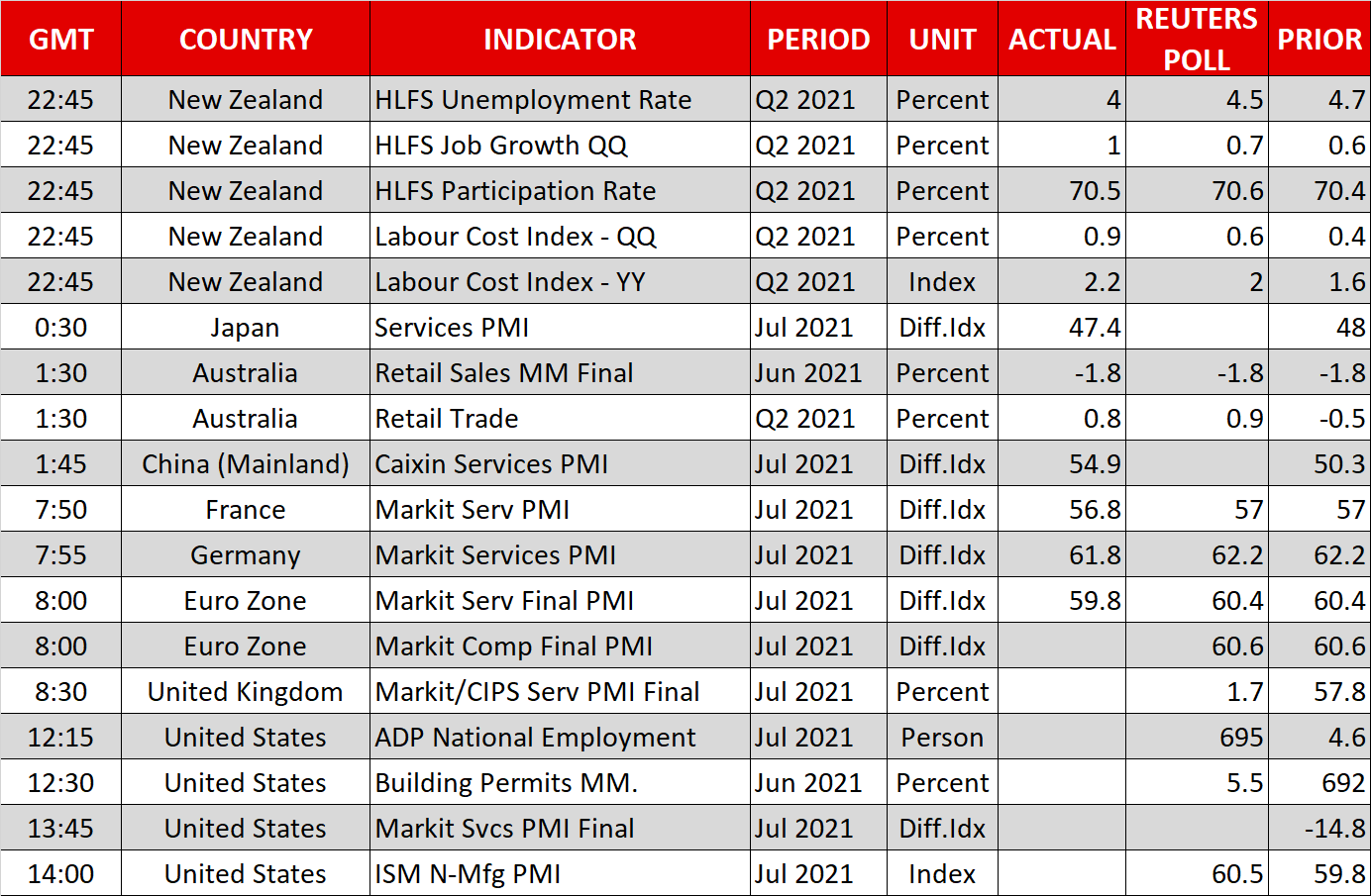

Speaking of normalization, the Reserve Bank of New Zealand will probably be the first major central bank to raise interest rates this cycle. The nation’s jobs data for Q2 were released overnight and crushed expectations, sealing the deal for a rate increase in two weeks.

In fact, markets are now pricing in a minor probability for a ‘double’ rate increase of 50 basis points this month. Almost three RBNZ rate increases have been baked into the cake by November. The economy is booming, the housing market is on fire, and the island nation remains virtually virus-free.

If the RBNZ is truly as aggressive as markets believe, the kiwi could be the next king of the FX market. The only missing ingredient is a rosier global environment. New Zealand is a small export-heavy economy after all, so its fortunes are ultimately tied to the global economy. The kiwi will probably be the biggest beneficiary should global growth worries fade a little.

Gold quiet, oil drops, US data coming up

In commodities, gold has been absolutely lifeless this week despite some favorable macro developments. Real US yields have been demolished and the dollar has been a shade softer, and yet bullion has been unable to capitalize.

That’s disappointing. If gold couldn’t stage a powerful rally with real yields falling apart, it could really struggle once the Fed takes its foot off the accelerator, especially if the dollar comes back swinging. As the old adage goes, if something can’t rally on good news, it probably won’t rally at all.

In energy markets, oil prices took another hit yesterday. Investors seem to be repricing the demand outlook as the Delta outbreak threatens to kneecap emerging market economies and perhaps even hamstring China. That’s happening against the backdrop of steady supply increases from OPEC.

As for today, some US events will keep dollar traders busy. The ADP jobs report will set expectations ahead of Friday’s nonfarm payrolls, but even more crucial will be the employment sub-index of the ISM services survey. Meanwhile, a speech by Fed Vice Chairman Richard Clarida at 14:00 GMT will be watched closely for any hints that tapering is drawing closer.

XM.COM Review

Wednesday, 04 Aug, 2021 / 9:04